Euronext publishes Q1 2023 results

Eurocommercial Properties N.V. lists on Euronext Milan

Behind the scenes: migrating Borsa Italiana Equities and ETFs to Optiq®

On 27 March 2023, Euronext completed the migration of Borsa Italiana’s Equity and ETFs to the Optiq® platform – only nine months after the successful migration of the Euronext Core Data Centre from the United Kingdom to Italy. In this article, we look at how the teams worked behind the scenes to accomplish the most significant phase of the Optiq® migration just 22 months after Borsa Italiana joined Euronext, and how the Italian market’s presence on the Optiq® platform benefits all Euronext’s investors.

Close cooperation with clients a key success factor

According to Camille Raizin, Head of Transformation and Projects in Euronext’s Market Services (EMS) department, good internal preparation, clear guidelines and strong client relationships supported by the commitment of dedicated teams internally were key to manage a migration of this size and complexity.

Our aim was minimum disruption, to make a very complex process as smooth and clear for our clients as possible.

“We always want to take as much of the burden off clients as we can, by ensuring they are absolutely aware of what they need to do and of any changes on our side that might impact them,” she says. “Experience has demonstrated that clients prefer us to be in regular contact, and are happy to put up with us chasing them to avoid missing a crucial milestone in the process.”

To help clients keep abreast of the project’s progress and status, Euronext set up a full structure and organisation internally dedicated to client readiness. A dedicated Optiq® migration client-facing team was created with team members in Italy, France and the Netherlands, and dedicated tools implemented, including a shared tracker that ensured everyone was up to speed. The team mapped out the customer journey in close detail, so that this could be shared with clients and everyone was working from the same base.

Once the onboarding strategy had been defined, the migration team began an extensive programme of communication. They held client readiness webinars with clients across Europe, going through technical, logistical and functional changes. Multiple one-on-one meetings and regular phone calls were held between Euronext teams and the technical and business contacts from each client firm. These sessions made sure everyone was apprised of deadlines and deliverables at each project phase. And over fifty communication documents were also sent to clients and made available on the Euronext customer portal.

Given the migration’s wide impact, keeping to the tight migration schedule was essential. “Clients needed to secure time, resources and budgets, as well as make sure they had the needed capacity for IT work, weekend testing and so forth,” explains Simona Cervi, Head of Client Services and Membership in Euronext Market Services, Italy. “And, of course, if certain elements were missed it could delay the entire schedule. So, nothing could be left to chance. We had more than 20 steps to be checked for each client before we could say a client was ready.” Thanks to these extensive preparation efforts, and the teams’ deep knowledge of the clients, their business and technical set-ups, the phase one migration was completed successfully.

Dress rehearsals provide final check and peace of mind

In the weeks leading up to the go-live date, Euronext conducted two mandatory Dress Rehearsals for customers, both held on a Saturday. “During a Dress Rehearsal, a real trading day is replicated on the full set of financial instruments on all impacted markets. Over the course of the day, clients enter orders and execute trades to check that everything is working correctly,” Simona Cervi says. Clients had a team present during each rehearsal and over the migration weekend to run testing on their connectivity and access to the trading system.

On the Euronext side, technical, business and sales teams worked closely together to make sure clients had completed the necessary steps (including signing contracts, requesting access rights, functional and technical tests, etc.) to be able to participate in the dress rehearsals.

“In fact, this was so successful that the first customer dress rehearsal saw our best ever result, with a 99% success rate based on our KPIs on the first Saturday alone,” says Camille Raizin. “When we collected feedback after the phase one migration, customers told us how helpful our approach was, highlighting our communication, interaction and regular meetings and calls as key success factors. And we are learning as we go, so we hope to make it even better for phases two and three.”

Bringing the benefits of Optiq® technology to the Borsa Italiana markets

Now that this first phase of the migration is complete, a world of benefits opens up for the Italian capital markets. “By joining Europe’s largest liquidity pool, we are further strengthening Italian capital markets. This migration will bring significant benefits to Italian issuers, members, investors and the real economy, as well as to the European financial markets ecosystem,” comments Fabrizio Testa, CEO of Borsa Italiana and Head of Fixed Income Trading. Italian professional and private investors will benefit from a state-of-the-art platform, gain access to a wider range of European equities and ETFs and a range of complementary features and services, such as Best of Book and Internal Matching Services. At the same time, Euronext has updated the Optiq® platform to accommodate existing trading services Borsa Italiana offered to the Italian market, such as Trading After Hours, the Market for Investment Vehicles and direct distribution and takeover bids. Borsa Italiana’s market issuers also benefit from this migration, as they now have seamless access to a considerably larger number of investors, a larger network of trading participants and to superior market quality.

Bringing the benefits of the Borsa Italiana markets to Euronext investors everywhere

Manuel Bento, Group Chief Operating Officer at Euronext, also points out that the migration benefits go far beyond the Italian market.

Euronext adopts the best practices of both the Borsa Italiana and Euronext markets, maintaining key local specificities that have strong market value and harmonising these across markets wherever relevant. Thus, all our clients will be able to benefit from the enhanced features this migration provides.

Euronext investors now have a whole new market to trade, accessible simply by extending their membership. And features from the Borsa Italian trading platform – such as strategy trading, post-trade management and public distribution – will now be incorporated in the Optiq® platform to benefit all Euronext investors.

The Optiq® migration offers ESG-related benefits as well. “Each time we have migrated an exchange to Optiq®, we have reduced our server footprint,” explains Manuel Bento. “When combined with the replacement of other servers and devices with more efficient ones, this has resulted in a 10% reduction in our overall carbon footprint. The fact that Optiq operates from our new core data centre in Bergamo – powered by 100% renewable sources – will positively impact not only our carbon footprint, but our clients’ as well, which now includes our clients in Italy.”

Past migration experiences indicate best is yet to come

When Euronext first launched its proprietary Optiq® trading platform in 2018, it initially went live in four Euronext markets. As Euronext continued to expand the platform to other markets, the benefits of operating on a shared platform became increasingly apparent. “Euronext has a strong track record of integrating exchanges onto our Optiq® platform,” says Chris Topple, Head of Global Sales at Euronext and CEO of Euronext London. “We integrated the cash markets of Euronext Dublin in 2019, and the cash, fixed income and derivatives markets of Oslo Børs in 2020. In both cases, the exchanges experienced an increase in client membership post-migration, as well as increased trading volumes due to the markets opening up to more members and investors, contributing to local market growth and expansion. Thus, we fully expect that this migration will increase Borsa Italiana’s member base and expand the service and product offerings to clients.”

Chris Topple also highlights how harmonisation benefits Euronext and its clients. “Using the same technology for all our cash and derivatives markets means that design and architecture are harmonised, simplifying development and maintenance for both our company and our clients. And we of course continuously work closely with our clients to optimise how they use the platform and support them in making the most of its technological advantages.”

Phase two already underway

Before the completion of the first migration phase, the Euronext migration team had already begun working on phase two, which will migrate fixed income, warrants and certificates to the Optiq®

platform in the third quarter of 2023. The third and final migration phase will cover financial derivatives and commodities and is scheduled for the first quarter of 2024.

Concurrently, Euronext is continuing the expansion of Euronext Clearing to all its markets, with cash equities planned for the fourth quarter of 2023 and financial derivatives and commodities in the third quarter of 2024. "Moving forward, Euronext Clearing will become Euronext’s CCP of choice for its cash equity, listed derivatives and commodities markets, providing a harmonised clearing framework across Euronext venues,” Chris Topple says. “This will allow us to directly manage a key client service and provide a harmonised, reliable clearing framework across all our trading venues. Clients will be able to benefit from cross-margining, balancing all their trading activities in each asset class across six markets. When combined with our single liquidity pool, trading platform and order book, this level of harmonisation will enable us to improve end-to-end efficiency and address market fragmentation, for the benefit of all our clients."

| The Optiq® trading platform in numbers |

|---|

|

| New digital tools for clients |

|---|

|

Euronext client services are being enhanced with a digital transformation programme based on the new MyEuronext customer portal. The new digital system empowers clients with:

Even more services should be up and running for phases two and three of the migration. |

ReFuels lists on Euronext Growth Oslo

Quality of execution comparison between FX Global Code signatory and Non-Code signatory liquidity providers across Euronext FX

Pages: 27

Publication: 30 November 2022

Authors: Paul Besson, Head of Quantitative Research and Mehdi-Lou Pigeard, Quant Research Analyst

FX Global Code/Non-Code Assessment - Let Data Drive your Decision

Quality of execution comparison between FX Global Code signatory and Non-Code signatory liquidity providers across Euronext FX

In this paper, we compare the Spot FX liquidity on the Euronext FX and Euronext Markets Singapore platforms (together, Euronext FX) between liquidity providers that have signed up to the FX Global Code (Code makers) versus liquidity providers that have not signed up to the Code (Non-Code makers). Based on trades executed on Euronext FX, Code makers overall bring better quality of execution than Non-Code makers. Nevertheless, the analysis also shows that in 25% of cases, Non-Code makers improve the quality of the liquidity on Euronext FX compared to Code makers.

We first evidence that Non-Code makers account for 32% of the turnover on all crosses (see Table 2, p.5). We further show that no significant differences are observed between Code and Non-Code makers on a taker’s realised spread (see Table 3, p.7) and Markouts (Table 4 and Table 5, p.9). This dispels the preconception that Non-Code makers would display more leakage and larger Markouts.

We then show that Non-Code makers have a +12% higher rejection rate than Code makers (Table 6, p.11) on all crosses.

Lastly we evidence that Non-Code makers have a +0.12 bps larger expected slippage than Code makers (see Table 8 p.17) on all crosses. However, we further clearly show that in 25% of sessions, Non-Code makers have a better expected slippage compared to Code makers (see Table 8, p.17).

These conclusions support our view that, at this time, the most efficient response to the Code / Non-Code choice is for takers on our platforms to make a data driven decision regarding the make-up of their liquidity pool. To support this choice, we encourage our takers to perform an ongoing case-by-case assessment of their makers on Euronext FX.

Main questions on Code makers addressed

In light of the recent changes to the FX Global Code and increasing industry adherence, Euronext FX has taken a pragmatic stance, evaluating the pros and cons of its Code makers versus its Non-Code makers.

In this paper, we will provide answers to the following questions:

- How does the liquidity brought by Non-Code makers compare to that brought by Code makers?

- Are spreads higher with Non-Code makers compared to Code makers?

- Is there more leakage when trading with Non-Code makers compared to Code makers?

- Are Non-Code makers rejecting trades more often than Code makers? And at a worst timing?

- How can we assess the benefits brought by a maker from the taker’s point of view: the expected slippage?

- Are Non-Code makers worsening the taker’s slippage, on average? How often in this case?

To answer these questions we will study empirically the outcomes for a taker trading in anonymous sessions. We will measure from the taker point of view the consequences of trading with a Code maker or Non-Code maker.

FX Global Code vs Non-Code Webinar

Watch the video of our Quant Research and FX teams explaining key results and answering a variety of quant, policy and liquidity management questions, to enable market participants to make data-driven choices.

- Is there a measurable difference in the quality of execution between Code signatory and Non-Code signatory LPs?

- How did this research drive Euronext FX's latest policy decision around the Code?

- What trends have we seen in Code adherence of market participants on the platform?

- And much more

Digital Value transfers to Euronext Milan

From better Markouts to better passive execution prices on Primary Markets compared to MTFs

Pages: 28

Publication: 6 October 2022

Authors: Paul Besson, Head of Quantitative Research, Théo Compérot, Quant Research Analyst and Cheng-Feng Gu, Quant Research Analyst

In this note we show that the timing of passive trades is directly connected to overall passive execution prices, thereby connecting Markouts and passive execution prices.

We first evidence that the average passive selling price on Euronext is +0.60 bps higher than on Cboe, and +0.56 bps higher than on Turquoise (see Figure 4, p10).

We also show that unfavourable market timing for a passive trade is more likely (+6%) on Cboe and on Turquoise than when considering all venues together. Further, we evidence that favourable market timing is less frequent (-4%) on Cboe and on Turquoise than when considering all venues (see Figure 7, p13).

We recommend that the favourable price improvements seen for passive trading on Primary Markets should be taken into account explicitly by Smart Order Routers.

From Markouts to passive trading prices

Bridging Markouts and passive execution prices

While the relationship between Markouts1 and adverse selection for a passive trader is well established, a worse Markout is often not considered by traders to be as detrimental as a worse execution price. This misconception arises from the fact that passive trades are always executed at a predetermined limit price, leading to a perception that the timing of the trade does not necessarily impact overall passive trading prices. In this note we show that the timing of passive trades is directly connected to overall passive execution prices, thereby connecting Markouts and passive execution prices.

How adverse timing selection leads to worse passive execution prices

We consider two traders with different Markouts over the same trading period. This difference in Markouts corresponds to a difference in the timing of the trades. The difference in trade times naturally leads to a difference in trading prices.

For this reason, when comparing two passive sellers, we would intuitively expect that the passive seller that has a smaller Markout and can avoid selling before a large price rise, would sell on average at a higher price than the participant that displays a larger Markout, and is therefore more likely to sell before the price rises.

Main questions addressed on Markouts and passive execution prices

In order to uncover the link between Markouts and passive trading prices we will provide answers to the main four questions below:

- How can we objectively assess the outcome of a passive trade on a given venue?

- Are average passive execution prices more attractive on Primary Markets versus MTFs?

- Do passive trades on MTFs take place at a worse market timing compared to passive trades on Primary Markets?

- Do worse Markouts and market timing lead to worse Passive VWAP prices on MTFs versus Primary Markets?

We will study the case of a passive seller over a 5-minute time interval. We consider the outcome of passive sells on the main Lit continental venues: Euronext, Cboe, Aquis and Turquoise. We show that venue choices lead to significant differences in outcomes and we relate these findings to the differences in Markouts across exchanges.

1 For more details on Markouts, see our February 2022 Quant Note “Better passive posting across Lit venues based on quantitative analysis of Markouts” available on https://www.euronext.com/en/quant-research

Request the report, contact us: QuantReports@euronext.com

Euronext announces volumes for April 2023

Euronext Eurozone SBT 1.5 Index

The first Eurozone climate-oriented index part of the SBT Family.

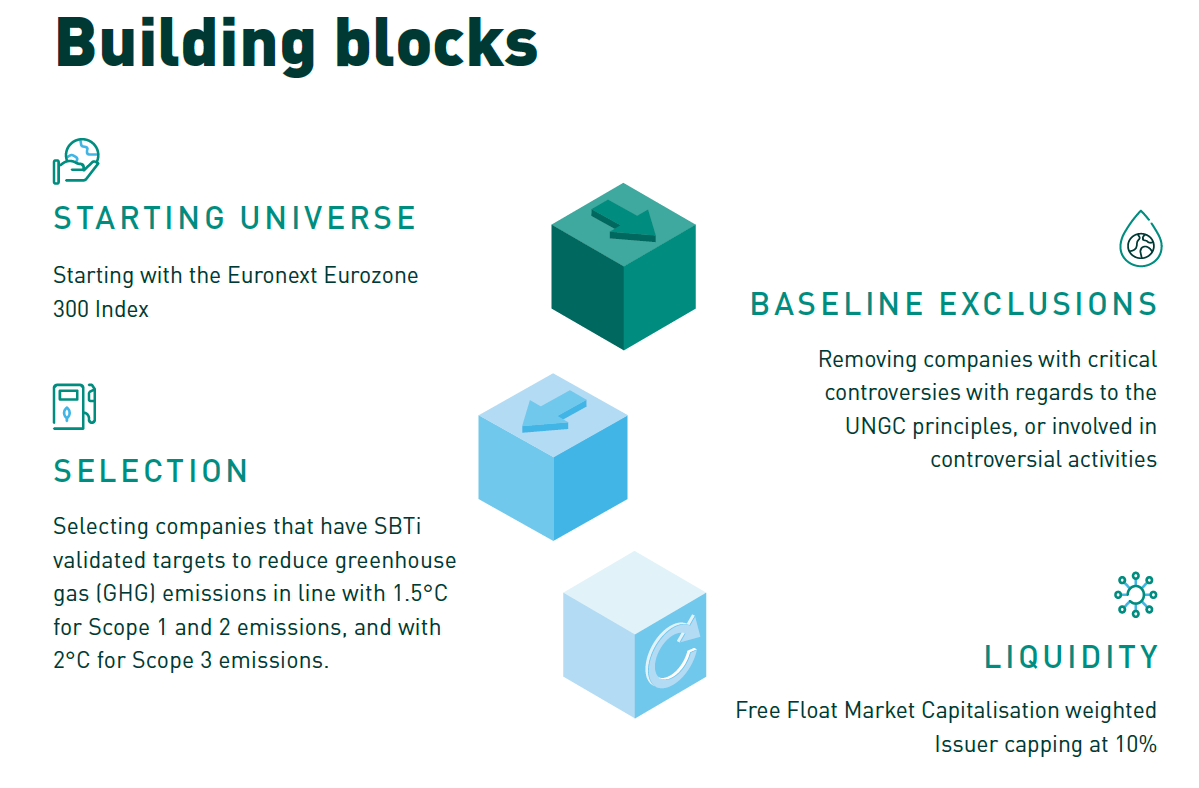

The SBT family includes several indices validated by the SBTi. The Science Based Targets initiative (SBTi) helps companies to set ambitious corporate climate action. It aims to lead the way to a zero-carbon economy, boost innovation and drive sustainable growth by setting science-based emissions reduction targets.

Key principles of the Eurozone SBT 1.5 Index

Companies facing an ESG controversy rating of category High or Severe, or that are not compliant with the UNGC principles, as assessed by Sustainalytics, are not eligible for the index.

Exclusion of companies based on temperature assessment is also applicated.

From the Index Universe, the Companies with any of the following characteristics are not eligible: Tobacco Products Production and related products/services, Tobacco Products Retail, Controversial Weapons, Shale Energy Extraction, Oil Sands Extraction, Arctic Oil & Gas Exploration Extraction, Thermal Coal Extraction, Thermal Coal Power Generation, Small Arms Civilian customers.

This index offers opportunities for a large range of investment vehicles such as ETFs, funds and structured products.

Learn more about the Euronext Eurozone SBT 1.5 Index:

Eurozone SBT 1.5 Index Rules | Eurozone SBT 1.5 Factsheet

Eurozone SBT 1.5 ESG Report | Eurozone SBT 1.5 Index Brochure | View the EU/EZ SBT 1.5 Indices Press Release

Euronext offers other SBT and ESG Blue-Chip indices:

Discover the CAC SBT 1.5 Index | Discover the Euronext Europe SBT 1.5 Index

Discover more Euronext ESG Blue-chip Indices

Watch the presentation:

Contact us at index-team@euronext.com for any queries.

Back to previous page | Euronext Index Data Page | Euronext Index Team Services

Gross trade prices on Italian stocks on Borsa Italiana outperform Equiduct APEX

Pages: 16

Publication date: 13 March 2023

Authors: Paul Besson, Head of Quantitative Research, Théo Compérot, Quant Research Analyst and Anatole Casimir, Quant Research Analyst

In this note we compare the relative performance of aggressive executions on Italian stocks, by comparing Lit trades on Borsa Italiana with trades on Equiduct MTF. To conduct this assessment we compare gross executions with the Primary Best Bid Offer prices. Our analysis is based on public market data from independent data provider BMLL, and is fully reproducible.

We first evidence that, when considering all trades from Equiduct APEX, retail gross trade prices on Italian stocks are worse than those on the Primary Market of Euronext Milan by -1.60 bps (see Table 4, p9).

Likewise we also show that, through Euronext’s Best of Book retail programme, Best of Book gross trade prices improve Primary Market quotes by +0.96 bps (see Table 5, p10).

Comparing retail executions on Primary Markets and on Equiduct (APEX)

On the Legacy Euronext Markets, retail traders can trade via the Best of Book model (later referred to as BoB), which enables aggressive orders from retail brokers to interact with specific retail quotes provided by designated market makers that supplement the all-to-all liquidity of the Euronext orderbook.

Another alternative for retail providers is to use the Equiduct APEX model (later referred to as EQDT), which allows aggressive retail traders to trade at the consolidated volume weighted at the best limits as computed by Equiduct (VBBO).

In order to compare the outcomes of these two models, we compute for each trade its Primary improvement versus the Primary Best Bid Offer. Thus we compare the Primary improvements offered by Equiduct and by Euronext Best of Book.

On Italian stocks, since orders are not specifically identified as retail orders on Euronext Milan, we compare Equiduct APEX retail trades with standard Lit aggressive trades on Milan market (later referred to as XMIL, its MIC code). We then compare the Gross and Net Primary improvements of these trades.