The national ESG blue-chip index dedicated to the french market.

Serving as the new French ESG index reference

To continue supporting the growing demand for investment solutions with ESG considerations, Euronext has designed a new ESG version of the Euronext’s iconic CAC 40® Index: the CAC 40 ESG® Index.

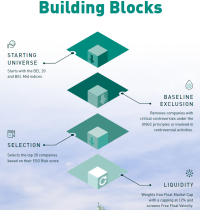

The CAC 40 ESG® Index is designed to direct capital flows of the top 40 French companies within the CAC® Large 60 index demonstrating the best Environmental, Social and Governance (ESG) practices.

CAC 40 ESG Index methodology

The CAC 40 ESG® index is designed to direct capital flows of the top 40 French companies within the CAC® Large 60 index demonstrating the best Environmental, Social and Governance (ESG) practices.

The index methodology follows the principles of the SRI label, implementing robust socially responsible investment principles.

Companies reported as controversial under the UN Global Compact are excluded (companies with involvement in coal mining, coal-fueled power generation (>10% turnover), tar sand & oil shale extraction and civilian, firearms (>10% turnover) and controversial, weapons. Distribution of tobacco is also excluded).

The CAC 40 ESG® offers opportunities for the creation of a large range of investment vehicles such as ETFs, funds and structured products.

Learn more about CAC 40 ESG:

CAC 40 ESG Index Rules | CAC 40 ESG Index Factsheet

CAC 40 ESG Report | CAC 40 ESG Press Release

Invest in the CAC 40 ESG Index

The CAC 40 ESG Index offers great opportunities for ETFs already proposed by BNP Paribas and Amundi.

The CAC 40 ESG® Index also offers investors futures on the CAC 40 ESG® Index.

Learn more about cac 40 ESG Future

Watch the presentation:

Euronext ESG Blue-chip indices

The CAC 40 ESG® Index is a key component of a broader suite of flagship ESG indices.

Discover more Euronext esg blue-chip Indices

Contact us at index-team@euronext.com for any queries.

Back to previous page | Euronext Index Data Page | Euronext Index Services