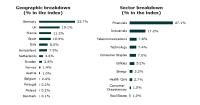

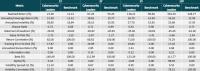

What is the Euronext Listed Private Equity Index?

The Euronext Listed Private Equity Index provides investors with exposure to the world’s leading private equity firms through their publicly listed shares. Instead of investing directly in early-stage private companies, this index allows investors to participate in the growth of firms that source, fund, and scale the next generation of high-growth businesses across artificial intelligence (AI), technology, industrials, and strategic infrastructure.

Key insights: private equity and the AI revolution

- Early AI access through private equity

Private equity firms such as KKR, CVC, and EQT are backing major AI innovators like Mistral and Anthropic long before these companies reach public markets, giving investors early exposure to the AI ecosystem. - Rate cuts accelerate deal flow

As central banks lower interest rates, private equity firms are deploying capital more rapidly, scaling AI and technology-driven platforms in a more favourable financing environment. -

Strategic industries in focus

Private equity investment is concentrated in critical sectors including semiconductors, industrial automation, defence, and digital infrastructure, supporting the backbone of future economic growth.

How the index works

The Euronext Listed Private Equity Index tracks the performance of publicly traded private equity firms that are actively investing in transformative sectors. These firms are the architects of innovation, deploying billions into industries that shape the future well before public markets catch up. While public investors often focus on mega-cap tech stocks, private equity firms are building the infrastructure and enablers of AI at earlier stages, supporting companies like Mistral (large language models), Anthropic (safe AI), and AI-native industrial platforms.

The impact of rate cuts and market trends

Recent rate-cutting cycles by central banks have reignited mergers and acquisitions activity. With lower financing costs and abundant capital, private equity firms are accelerating acquisitions, carve-outs, and the scaling of growth platforms. This environment is particularly favourable for expanding AI and technology-driven businesses.

Private equity’s role in strategic sectors

Amid geopolitical shifts and rising protectionism, Europe is prioritising investment in critical technologies such as semiconductors, cloud infrastructure, defence, and automation. Private equity firms are key players in this transformation, providing the capital and expertise needed to scale strategic industries and build resilient digital and industrial infrastructure.

Contact the team at index-sales@euronext.com for more information